Dutch finance company

Like the holding company, the Dutch finance company is a worldwide renowned and frequently used instrument in tax planning. Any Dutch tax resident legal entity and corporate income tax subject is eligible for the financing regime. A company’s main purpose could be financing (group) companies by providing loans, but in many cases a holding company takes care of the group’s financing function as well.

Why choose a Dutch finance company?

The main advantages of a Dutch finance company and the reasons why the Netherlands are the jurisdiction of choice for financing and licensing vehicles:

- The Netherlands does not impose withholding taxes on interest (and royalty) payments

- The Netherlands has entered into over 90 tax treaties providing for reduced withholding taxes on incoming interest and royalty payments. In addition, EU Directives provide for 0% on dividend, interest and royalty payments to the Netherlands.

- An advance pricing agreement (tax ruling possible) is possible for financing activities, whereas an arm’s length spread to be reported at the level of the finance company is taxed. See our topic advance pricing agreements at our section tax facilities for more on this.

- Costs are deductible

- Effective tax rate can be very low

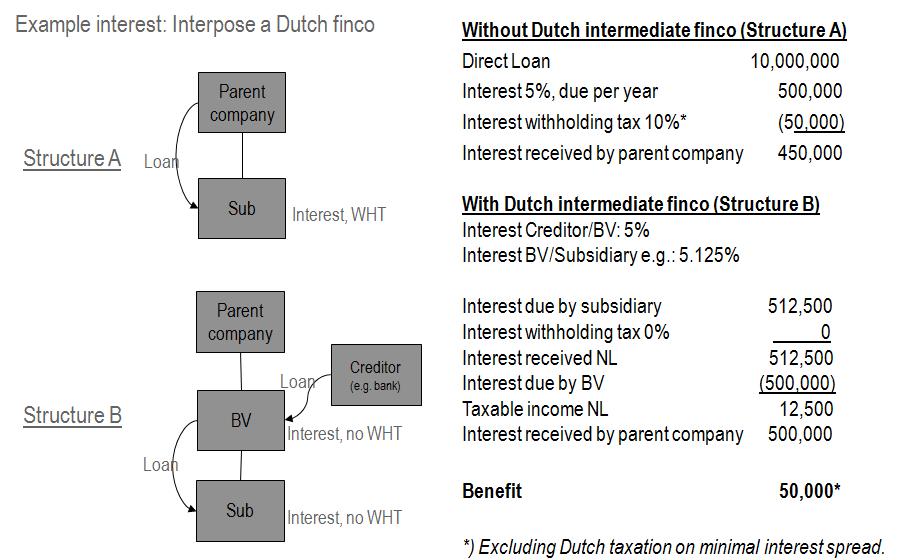

Below we provide an example of how the interposition of a Dutch finance company can lower the effective tax burden (click to enlarge).

New: group Interest box

Dutch law contains a new facility whereas income from qualifying group financing activities is taxed effectively at a rate of 5%. Although enacted, the provision still is not effective. The facility would make the outstanding Dutch finance regime even more competitive. Keep a close eye on this section for more on this.

Hybrid debt instrument

A tax efficient way to leverage foreign group company could be the usage of hybrid debt instruments.

High Level Steps

The Dutch financing company provides a hybrid debt instrument to a qualifying shareholding or group company in amongst other (but not limited to) the following jurisdictions: Australia, Belgium, Brazil, Canada, China, Finland, France, Georgia, Greece, Hungary, India, Israel, Japan, Malaysia, Poland, Portugal, Romania, Russia, Senegal, Singapore, South Korea, Spain, Switzerland, United States

The benefits are as follows:

- Interest deduction at the level of the borrower for local tax purposes.

- Interest income received on the hybrid debt instrument should be exempt at the level of the Dutch lender under the Dutch participation exemption regime.

Considerations

- Qualification of borrower for Dutch participation exemption

- Foreign qualification of hybrid debt instrument

- Changes in legislation, case law or policy since the moment of development of the hybrid need to be reviewed on a case by case basis and might result in the hybrid no longer being feasible from a Dutch or foreign tax or legal point of view

- No credit for foreign interest withholding tax under NL participation exemption

- Foreign CFC legislation

We have vast experience with setting up and implementing Dutch financing companies for our clients (see our sections company formation and tax structuring section for more on how we can help structure your business). In case you are interested in how a Dutch financing company can be of use for your business, please feel free to contact us.